import pandas

local_filepath = "train.csv"

data = pandas.read_csv(local_filepath)

data.sample()| row_id | date | country | store | product | num_sold | |

|---|---|---|---|---|---|---|

| 2025 | 2025 | 2017-02-12 | France | KaggleMart | Kaggle Getting Started | 291 |

Time series forecasting is one of the most important fields in statistics because it is arguably the most impactful for businesses. Every business would love to know what will happen tomorrow, next week, next year, and next 10 years and make decisions accordingly. Although statistical methods for forecasting is not quite the silver bullet, it can help us make reasonable predictions under certain assumptions.

In this post, we will look into several forecasting models - both classical methods (e.g. ARIMA) and deep learing (LSTM, CNN) - and compare their performance using hyperparameter optimization with Optuna. I will also assume a business case in the end and the best model will be the less costly one. Let’s start with some data analysis and visualizations.

Firstly we will import the training dataset train.csv using pandas and check its columns and some sample values.

import pandas

local_filepath = "train.csv"

data = pandas.read_csv(local_filepath)

data.sample()| row_id | date | country | store | product | num_sold | |

|---|---|---|---|---|---|---|

| 2025 | 2025 | 2017-02-12 | France | KaggleMart | Kaggle Getting Started | 291 |

data.describe()| row_id | num_sold | |

|---|---|---|

| count | 70128.000000 | 70128.000000 |

| mean | 35063.500000 | 194.296986 |

| std | 20244.354176 | 126.893874 |

| min | 0.000000 | 19.000000 |

| 25% | 17531.750000 | 95.000000 |

| 50% | 35063.500000 | 148.000000 |

| 75% | 52595.250000 | 283.000000 |

| max | 70127.000000 | 986.000000 |

# Check for missing values

True in data.isnull()FalseGood. The data don’t have any missing values. Now let’s check for what kind of values that the data have on each column.

print(f"Unique country values are: {data['country'].unique()}\n")

print(f"Unique store values are: {data['store'].unique()}\n")

print(f"Unique product values are: {data['product'].unique()}\n")

print(f"Unique dates are: {data['date'].unique()}\n")Unique country values are: ['Belgium' 'France' 'Germany' 'Italy' 'Poland' 'Spain']

Unique store values are: ['KaggleMart' 'KaggleRama']

Unique product values are: ['Kaggle Advanced Techniques' 'Kaggle Getting Started'

'Kaggle Recipe Book' 'Kaggle for Kids: One Smart Goose']

Unique dates are: ['2017-01-01' '2017-01-02' '2017-01-03' ... '2020-12-29' '2020-12-30'

'2020-12-31']

So the table has the daily sales data of 4 different books, sold in 2 different stores, which have branches in 6 different countries, spanning from start of 2017 to the end of 2020. Data has 70128 rows which means for each book, store and country combination we have 4 years of sales data.

Let’s plot a subset of the whole data.

import plotly.express as px

subsets = pandas.DataFrame()

subsets["subset1"] = data[

(data["country"] == "Germany")

& (data["store"] == "KaggleMart")

& (data["product"] == "Kaggle Advanced Techniques")

].set_index("date")["num_sold"]

subsets["subset2"] = data[

(data["country"] == "Belgium")

& (data["store"] == "KaggleRama")

& (data["product"] == "Kaggle Getting Started")

].set_index("date")["num_sold"]

subsets["subset3"] = data[

(data["country"] == "France")

& (data["store"] == "KaggleMart")

& (data["product"] == "Kaggle Recipe Book")

].set_index("date")["num_sold"]

fig = px.line(

subsets,

width=700,

height=500,

title="Sales Data For Different Subsets",

labels={"value": "Sales", "date": "Date", "variable": ""},

)

fig.show();Looking at the plot, especially in the Subset1, there is a yearly seasonality in the sales. Also there is a sharp rise in the sales around New Year’s Eve.

Before modelling, we have to check whether any extra data transformation is needed. Since the data has 48 subsets like the 3 subsets above, it has to be arranged such that a subset’s all values for 4 years are in a sequence before continuing to another subset. Let’s create a sample DataFrame to illustrate this point.

import numpy as np

sample_countries = ["Germany", "France"]

sample_stores = ["KaggleRama", "KaggleMart"]

sample_timepoints = [0, 1, 2, 3]

sample_num_sold = np.tile([10, 20, 30, 40], 4)

idx = pandas.MultiIndex.from_product(

[sample_countries, sample_stores, sample_timepoints]

)

example = pandas.DataFrame(index=idx, data={"num_sold": sample_num_sold})

example| num_sold | |||

|---|---|---|---|

| Germany | KaggleRama | 0 | 10 |

| 1 | 20 | ||

| 2 | 30 | ||

| 3 | 40 | ||

| KaggleMart | 0 | 10 | |

| 1 | 20 | ||

| 2 | 30 | ||

| 3 | 40 | ||

| France | KaggleRama | 0 | 10 |

| 1 | 20 | ||

| 2 | 30 | ||

| 3 | 40 | ||

| KaggleMart | 0 | 10 | |

| 1 | 20 | ||

| 2 | 30 | ||

| 3 | 40 |

Now transform the whole data.

from pandas import to_datetime

# First sort the data and drop the row_id column since we don't need it.

transformed_data = data.sort_values(by=["country", "store", "product", "date"]).drop(

columns="row_id"

)

# Change the date column to pandas Datetime

transformed_data["date"] = to_datetime(transformed_data["date"])

transformed_data = transformed_data.set_index(["country", "store", "product", "date"])

transformed_data| num_sold | ||||

|---|---|---|---|---|

| country | store | product | date | |

| Belgium | KaggleMart | Kaggle Advanced Techniques | 2017-01-01 | 663 |

| 2017-01-02 | 514 | |||

| 2017-01-03 | 549 | |||

| 2017-01-04 | 477 | |||

| 2017-01-05 | 447 | |||

| ... | ... | ... | ... | ... |

| Spain | KaggleRama | Kaggle for Kids: One Smart Goose | 2020-12-27 | 204 |

| 2020-12-28 | 212 | |||

| 2020-12-29 | 242 | |||

| 2020-12-30 | 239 | |||

| 2020-12-31 | 202 |

70128 rows × 1 columns

The data is ready to model. We will create several different models for forecasting: ARIMA, Regression with ARIMAX and XGBoost, and Deep Learning with Long Short Term Memory (LSTM). Each model may need another data transformation but it will be easy to transform from the data that we have already preprocessed.

We will not tune the hyperparameters rigorously at first, just enough to get reasonable forecasts. After we went through all of them, I will create a custom performance metric for an assumed business case and then we will compare each model according to this metric.

Autoregressive Integrated Moving Average (ARIMA) is a statistical method used for forecasting. It uses values at previous time points to predict current value (autoregression) and these regressions’ errors (moving average). Main assumption of ARIMA is that the time series should be stationary meaning its value is independent of time. Trend and seasonality makes the time series non-stationary. To make time series stationary we can use “differencing” - simply subtracting the value at t-1 from the value at t. “Integrated” part of the ARIMA is referring to the differencing order to make time series stationary.

ARIMA consists of three parts each having their own order - Autoregression p, Integration d, and Moving Average q. We will use Autocorrelation Function and Partial Autocorrelation Function graphs to select correct orders.

Moving to our data, just by looking the above plots we can say there is a strong seasonality in the time series but to quantify it we will use Kwiatkowski-Phillips-Schmidt-Shin (KPSS) test to check for stationarity.

from statsmodels.tsa.stattools import kpss

kpss_test = kpss(transformed_data)

print(f"p-value of KPSS test is: {kpss_test[1]}")p-value of KPSS test is: 0.01Null hypothesis of KPSS test is that the series is stationary. Since the p-value of our test result is smaller that 0.05 we can reject the null hypothesis and state that the series is non-stationary.

Before creating the ARIMA model we have to remove trend and seasonality from the data. We could use the seasonal variant of ARIMA called SARIMA; however, our data’s frequency is a day so it has a periodicity of 365 days. SARIMA models are more suitable for monthly or quarterly data; therefore we will use Seasonal-Trend Decomposition Using LOESS (STL) method to remove trend and seasonality from the data.

from statsmodels.tsa.seasonal import STL

import matplotlib.pyplot as plt

import pandas as pd

import seaborn as sns

# Setting plot style and size

sns.set_style("darkgrid")

plt.rc("figure", figsize=(7, 5))

plt.rc("font", size=10)

# Create a sample subset to plot

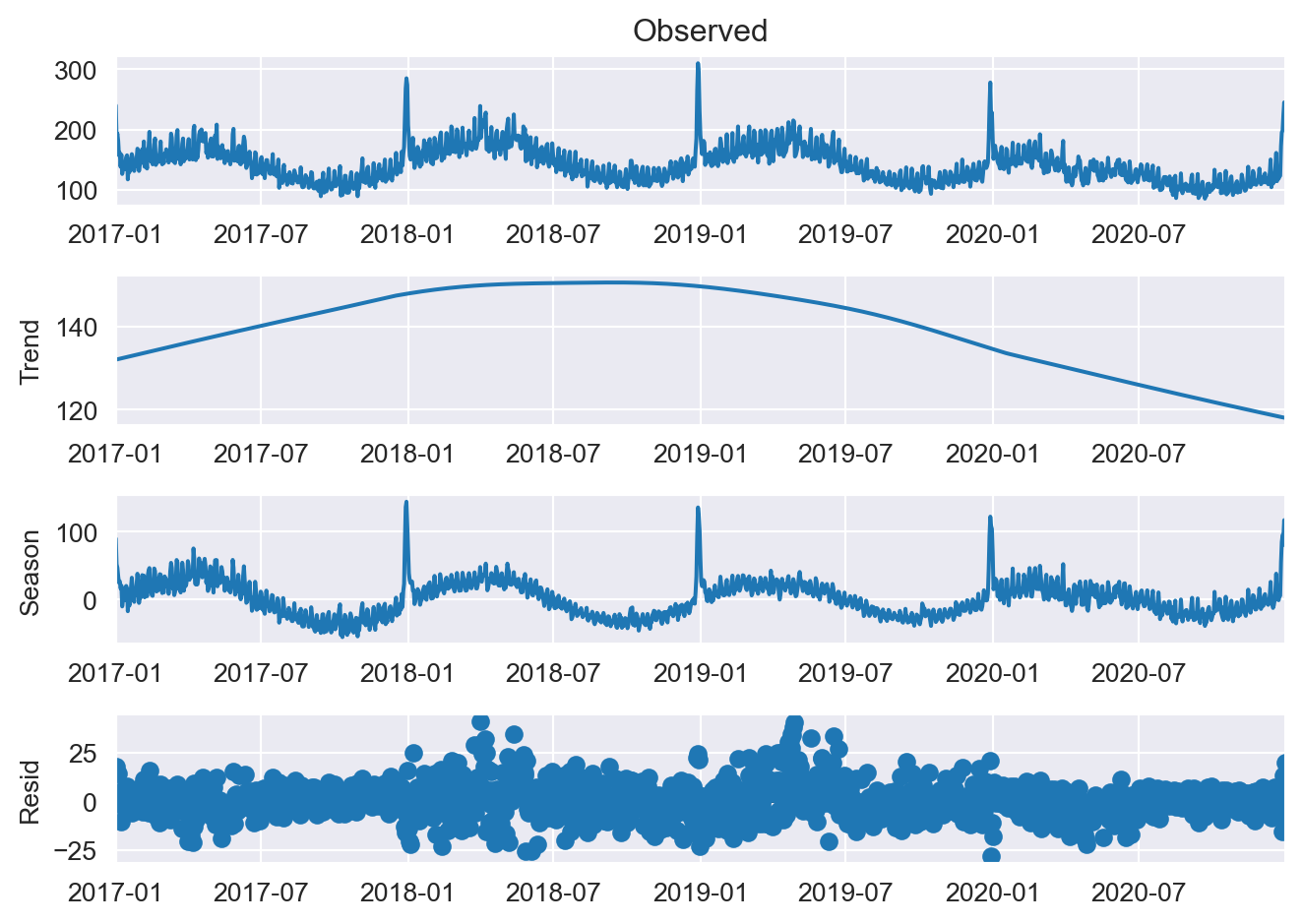

subset = transformed_data.loc["Germany", "KaggleRama", "Kaggle Advanced Techniques"]

# Plot the decomposed parts of the time series

stl = STL(subset, period=365, seasonal=7, trend_deg=1)

decomp = stl.fit()

fig = decomp.plot()

fig.show();

Above code decomposed the subset time series to three parts: trend, season, and residuals. Before creating ARIMA model, we still have to make sure that the residual part is non-stationary. We will test for stationarity with KPSS again and use differencing until it is stationary. This differencing degree will determine our I(d) parameter in the ARIMA model.

diff_test = kpss(decomp.resid)

print(f"p-value of KPSS test is: {diff_test[1]}")p-value of KPSS test is: 0.1Residual are stationary according to test so we won’t need a differencing in our model and therefore d degree will be 0. For the AR(p) order, we will look at the autocorrelation graphs. For the MA(q) order, we will try values and select the model with the lowest AIC (Akaike’s Information Criteria).

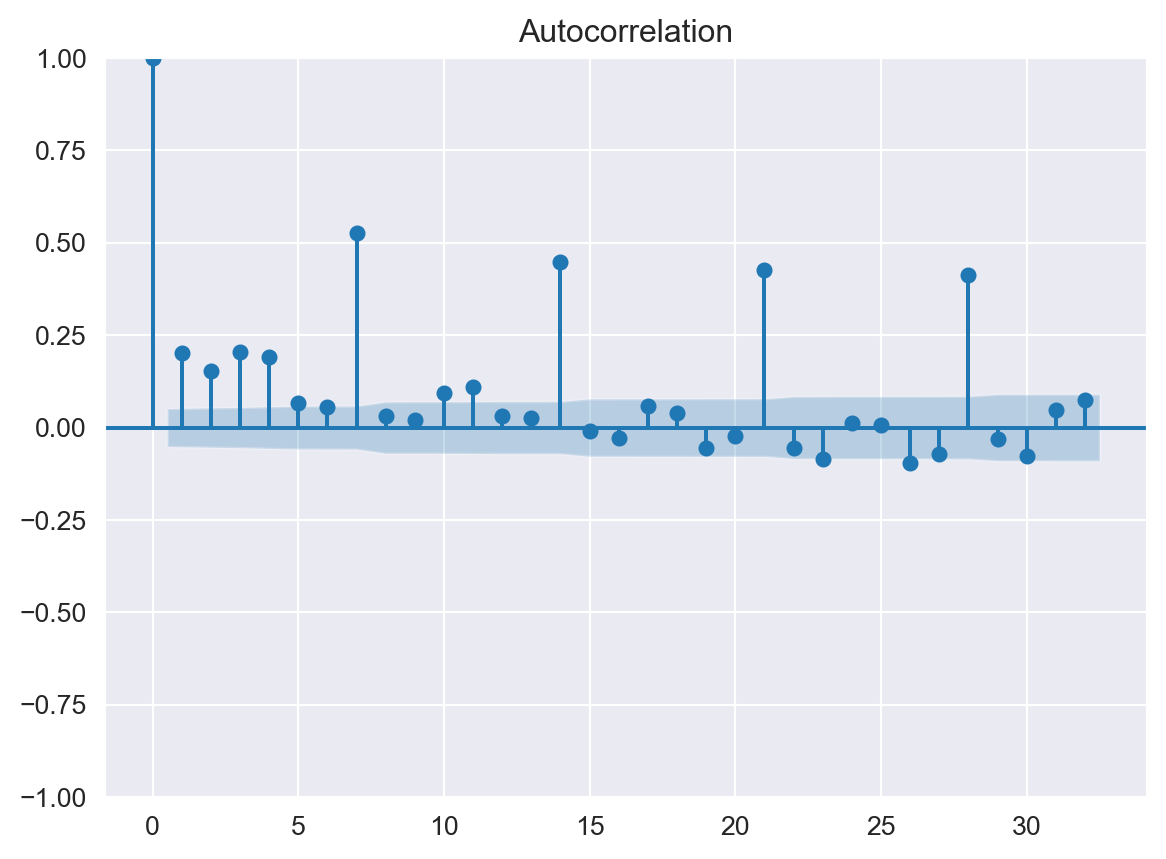

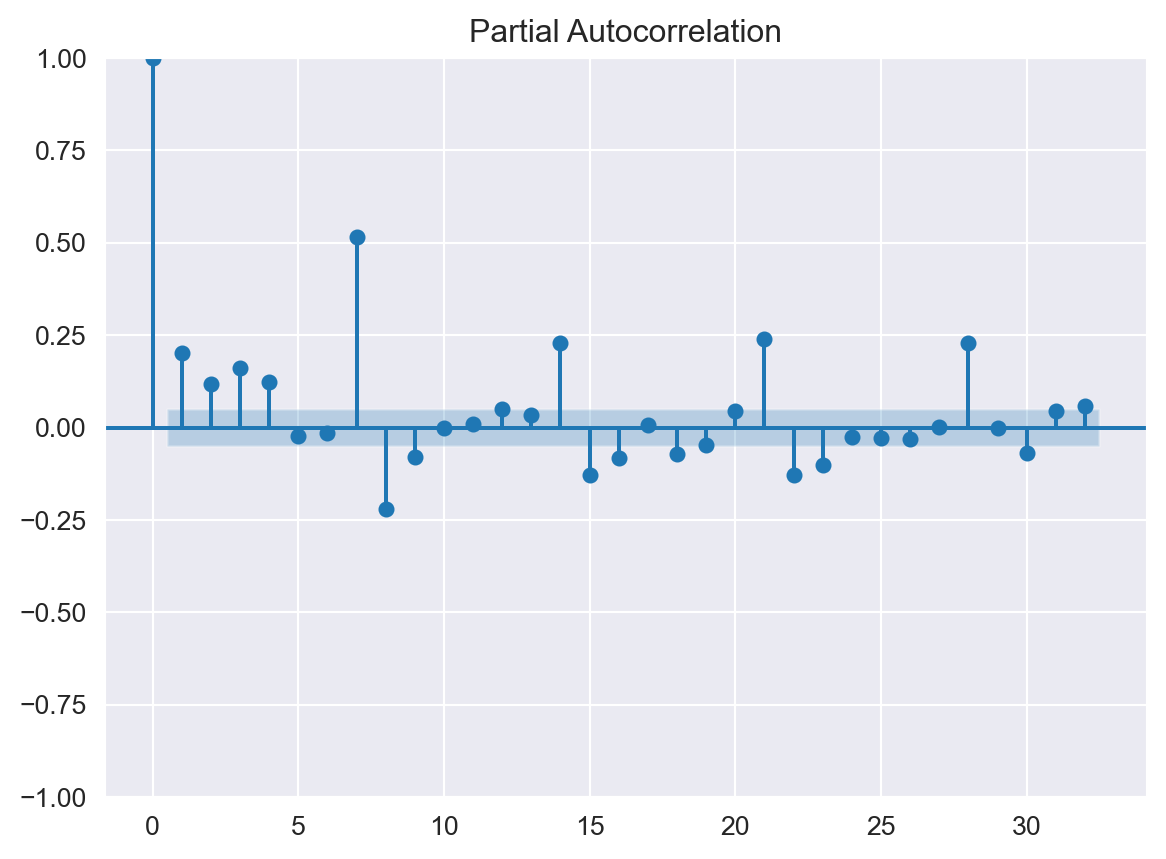

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

plot_acf(decomp.resid);

plot_pacf(decomp.resid);

Partial Autocorrelation Function shows statistically significant correlations at lags up to 7; thus we will start with AR(7). Now it is a good time to split our subset to train and test parts. Train data will be the first three years’ data and the test will be last year’s data.

from statsmodels.tsa.forecasting.stl import STLForecast, STLForecastResults

from statsmodels.tsa.arima.model import ARIMA

from sktime.forecasting.model_selection import temporal_train_test_split

# Split subset to train-test

train_subset, test_subset_pretuning = temporal_train_test_split(subset, test_size=366)

# Define STLForecast model

stl_forecast = STLForecast(

train_subset,

model=ARIMA,

model_kwargs={"order": (7, 0, 0), "trend": "t"},

period=365,

trend=1095,

robust=False

)

# Fit the model

model = stl_forecast.fit()

# Forecast for the last year

forecast = model.forecast(steps=366)

# Create a function to plot both test data and forecast from the model to compare them visually.

def plot_forecasts(y_true, y_pred, title="Forecasts", width=700, height=500):

# Create a DataFrame to store both series

series = pandas.DataFrame()

series["Observed"] = y_true

series["Predicted"] = y_pred

# Define plot attributes

fig = px.line(

series,

width=width,

height=height,

title=title,

labels={

"value": "Sales",

"variable": ""

}

)

fig.show()

plot_forecasts(test_subset_pretuning["num_sold"], forecast, title="STL-ARIMA Forecasts with (7,0,0)")

model.summary()| Dep. Variable: | y | No. Observations: | 1095 |

|---|---|---|---|

| Model: | ARIMA(7, 0, 0) | Log Likelihood | -3477.975 |

| Date: | Tue, 20 Dec 2022 | AIC | 6973.950 |

| Time: | 17:21:07 | BIC | 7018.937 |

| Sample: | 01-01-2017 | HQIC | 6990.973 |

| - 12-31-2019 | |||

| Covariance Type: | opg |

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| x1 | 0.0074 | 0.135 | 0.055 | 0.956 | -0.258 | 0.273 |

| ar.L1 | 0.1083 | 0.019 | 5.696 | 0.000 | 0.071 | 0.146 |

| ar.L2 | 0.1827 | 0.021 | 8.721 | 0.000 | 0.142 | 0.224 |

| ar.L3 | 0.1113 | 0.018 | 6.122 | 0.000 | 0.076 | 0.147 |

| ar.L4 | 0.1520 | 0.020 | 7.456 | 0.000 | 0.112 | 0.192 |

| ar.L5 | 0.0204 | 0.020 | 1.024 | 0.306 | -0.019 | 0.060 |

| ar.L6 | -0.0949 | 0.020 | -4.857 | 0.000 | -0.133 | -0.057 |

| ar.L7 | 0.5200 | 0.017 | 30.557 | 0.000 | 0.487 | 0.553 |

| sigma2 | 33.3182 | 0.864 | 38.550 | 0.000 | 31.624 | 35.012 |

| Ljung-Box (L1) (Q): | 8.57 | Jarque-Bera (JB): | 629.83 |

|---|---|---|---|

| Prob(Q): | 0.00 | Prob(JB): | 0.00 |

| Heteroskedasticity (H): | 1.06 | Skew: | -0.10 |

| Prob(H) (two-sided): | 0.60 | Kurtosis: | 6.71 |

| Period: | 365 | Trend Length: | 1095 |

|---|---|---|---|

| Seasonal: | 7 | Trend deg: | 1 |

| Seasonal deg: | 1 | Trend jump: | 1 |

| Seasonal jump: | 1 | Low pass: | 367 |

| Robust: | False | Low pass deg: | 1 |

The forecast looks pretty good already; however, from the summary we detect that p-value for Ljung-Box test is smaller than 0.05. The null hypothesis of Ljung-Box test is that residuals of the model after fitting ARIMA does not contain autocorrelations. Smaller than 0.05 p-value shows that our model could not capture the autocorrelations of the model fully. So will try different q orders and select the one which has the smallest AIC value and the case where the residuals are significantly autocorrelated (p > 0.05).

q_orders = np.arange(0, 8)

results = []

for q in q_orders:

stl_forecast = STLForecast(

train_subset,

model=ARIMA,

model_kwargs={"order": (7, 0, q), "trend": "t"},

period=365,

trend=1095,

robust=False,

)

model = stl_forecast.fit()

forecast = model.forecast(steps=366)

results.append(model.model_result.aic)

print(f"Best q is {results.index(min(results))} with AIC value of {min(results)}")Best q is 7 with AIC value of 6781.7431055363095Let’s check the summary again with q value of 7.

stl_forecast = STLForecast(

train_subset,

model=ARIMA,

model_kwargs={"order": (7, 0, 7),

"trend": "t"},

period=365,

trend=1095,

robust=False

)

model = stl_forecast.fit()

# Forecast for the last year

forecast = model.forecast(steps=366)

# Plot both test data and forecast from the model to compare them visually.

plot_forecasts(test_subset_pretuning["num_sold"], forecast, title="STL-ARIMA Forecasts with (7,0,7)")

model.summary()| Dep. Variable: | y | No. Observations: | 1095 |

|---|---|---|---|

| Model: | ARIMA(7, 0, 7) | Log Likelihood | -3374.872 |

| Date: | Tue, 20 Dec 2022 | AIC | 6781.743 |

| Time: | 17:21:19 | BIC | 6861.719 |

| Sample: | 01-01-2017 | HQIC | 6812.005 |

| - 12-31-2019 | |||

| Covariance Type: | opg |

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| x1 | 0.0307 | 0.042 | 0.725 | 0.468 | -0.052 | 0.114 |

| ar.L1 | -0.5356 | 0.018 | -29.124 | 0.000 | -0.572 | -0.500 |

| ar.L2 | -0.5941 | 0.025 | -24.214 | 0.000 | -0.642 | -0.546 |

| ar.L3 | -0.2172 | 0.022 | -9.847 | 0.000 | -0.260 | -0.174 |

| ar.L4 | 0.3197 | 0.016 | 19.906 | 0.000 | 0.288 | 0.351 |

| ar.L5 | 0.6246 | 0.022 | 28.755 | 0.000 | 0.582 | 0.667 |

| ar.L6 | 0.4675 | 0.024 | 19.285 | 0.000 | 0.420 | 0.515 |

| ar.L7 | 0.9349 | 0.018 | 52.310 | 0.000 | 0.900 | 0.970 |

| ma.L1 | 0.8207 | 0.022 | 36.479 | 0.000 | 0.777 | 0.865 |

| ma.L2 | 1.0375 | 0.034 | 30.775 | 0.000 | 0.971 | 1.104 |

| ma.L3 | 0.7876 | 0.045 | 17.633 | 0.000 | 0.700 | 0.875 |

| ma.L4 | 0.3276 | 0.046 | 7.110 | 0.000 | 0.237 | 0.418 |

| ma.L5 | -0.1245 | 0.040 | -3.140 | 0.002 | -0.202 | -0.047 |

| ma.L6 | -0.1949 | 0.029 | -6.761 | 0.000 | -0.251 | -0.138 |

| ma.L7 | -0.6672 | 0.021 | -32.522 | 0.000 | -0.707 | -0.627 |

| sigma2 | 27.4791 | 0.830 | 33.092 | 0.000 | 25.852 | 29.107 |

| Ljung-Box (L1) (Q): | 0.21 | Jarque-Bera (JB): | 359.53 |

|---|---|---|---|

| Prob(Q): | 0.65 | Prob(JB): | 0.00 |

| Heteroskedasticity (H): | 1.08 | Skew: | 0.07 |

| Prob(H) (two-sided): | 0.47 | Kurtosis: | 5.80 |

| Period: | 365 | Trend Length: | 1095 |

|---|---|---|---|

| Seasonal: | 7 | Trend deg: | 1 |

| Seasonal deg: | 1 | Trend jump: | 1 |

| Seasonal jump: | 1 | Low pass: | 367 |

| Robust: | False | Low pass deg: | 1 |

Finally calculate the mean absolute percentage error (MAPE) and R2 Score as a benchmark.

from sklearn.metrics import mean_absolute_percentage_error, r2_score

print(f"MAPE for STL-ARIMA model is: {mean_absolute_percentage_error(test_subset_pretuning, forecast)}")

print(f"R2 Score for STL-ARIMA model is: {r2_score(test_subset_pretuning, forecast)}")MAPE for STL-ARIMA model is: 0.18646794982275017

R2 Score for STL-ARIMA model is: -0.6091132358371121Now we will move to the forecasting which uses exogenous variables as features. To achieve that, firstly, we will convert the datetime of the series to tabular features and then add holidays. We will also use some libraries dedicated to feature extraction from time series.

For ARIMAX model, we will create a feature_matrix which has the date related features and lagged values as predictors.

import featuretools as ft

from sklearn.preprocessing import LabelEncoder, OneHotEncoder

import holidays

from statsmodels.tsa.deterministic import Fourier

# First we will create an EntitySet

entity_set = ft.EntitySet()

data = data.sort_values(by=["country", "store", "product", "date"])

# Specify index and time_index columns

entity_set.add_dataframe(

dataframe_name="Datetime Features",

dataframe=data,

index="row_id",

time_index="date",

)

feature_matrix, feature_defs = ft.dfs(

entityset=entity_set,

target_dataframe_name="Datetime Features",

trans_primitives=["DAY", "MONTH", "WEEKDAY", "YEAR"],

)

# Label encode the year column

year_encoder = LabelEncoder()

feature_matrix["YEAR(date)"] = year_encoder.fit_transform(feature_matrix["YEAR(date)"])

# Get the holidays for each country

holidays_country = [holidays.country_holidays(i) for i in data["country"].unique()]

# Add the original date column for comparison

feature_matrix["date"] = to_datetime(data["date"])

"""

Check dates for local holidays.

If there is a holiday on the date add their local name to holiday_name, else add "No Holiday".

"""

holiday_name = list()

for i in range(len(feature_matrix)):

if feature_matrix["country"][i] == "Belgium":

if feature_matrix["date"][i] in holidays_country[0]:

holiday_name.append(holidays_country[0].get(feature_matrix["date"][i]))

else:

holiday_name.append("No Holiday")

elif feature_matrix["country"][i] == "France":

if feature_matrix["date"][i] in holidays_country[1]:

holiday_name.append(holidays_country[1].get(feature_matrix["date"][i]))

else:

holiday_name.append("No Holiday")

elif feature_matrix["country"][i] == "Germany":

if feature_matrix["date"][i] in holidays_country[2]:

holiday_name.append(holidays_country[2].get(feature_matrix["date"][i]))

else:

holiday_name.append("No Holiday")

elif feature_matrix["country"][i] == "Italy":

if feature_matrix["date"][i] in holidays_country[3]:

holiday_name.append(holidays_country[3].get(feature_matrix["date"][i]))

else:

holiday_name.append("No Holiday")

elif feature_matrix["country"][i] == "Poland":

if feature_matrix["date"][i] in holidays_country[4]:

holiday_name.append(holidays_country[4].get(feature_matrix["date"][i]))

else:

holiday_name.append("No Holiday")

elif feature_matrix["country"][i] == "Spain":

if feature_matrix["date"][i] in holidays_country[5]:

holiday_name.append(holidays_country[5].get(feature_matrix["date"][i]))

else:

holiday_name.append("No Holiday")

feature_matrix["HolidayName"] = holiday_name

# Sort the dataframe so that date is sequential

feature_matrix = feature_matrix.sort_values(

by=["country", "store", "product", "date"], ignore_index=True

)

"""

Check for the closeness of days to holidays. If a day is in the spectrum of 3 days before -

3 days after of a holiday, label it as Close.

"""

holiday_closeness = list()

for i in range(len(feature_matrix)):

if feature_matrix["HolidayName"][i] != "No Holiday":

holiday_closeness.append("Holiday")

else:

if len(list("No Holiday" == feature_matrix["HolidayName"][i - 3 : i + 4])) == 0:

holiday_closeness.append("Close")

elif False in list(

"No Holiday" == feature_matrix["HolidayName"][i - 3 : i + 4]

):

holiday_closeness.append("Close")

else:

holiday_closeness.append("Distant")

feature_matrix["HolidayCloseness"] = holiday_closeness

# One-hot encode holiday closeness

feature_matrix = pandas.get_dummies(

feature_matrix,

columns=[

"country",

"store",

"product",

"DAY(date)",

"MONTH(date)",

"WEEKDAY(date)",

"YEAR(date)",

"HolidayCloseness",

],

drop_first=True,

)

# Deterministic Fourier Terms

## Yearly

yearly_fourier_terms = Fourier(365, 3)

index = np.arange(0, 1461)

yearly_fourier_terms = yearly_fourier_terms.in_sample(index)

cloning_func = lambda x: np.tile(x, 48)

yearly_fourier_terms = yearly_fourier_terms.apply(func=cloning_func, axis=0)

feature_matrix = feature_matrix.join(yearly_fourier_terms, how="left")

# Edit columns

feature_matrix = pandas.DataFrame.join(

feature_matrix.drop(columns=["num_sold", "HolidayName"]),

feature_matrix["num_sold"],

how="left",

)

feature_matrix| date | country_France | country_Germany | country_Italy | country_Poland | country_Spain | store_KaggleRama | product_Kaggle Getting Started | product_Kaggle Recipe Book | product_Kaggle for Kids: One Smart Goose | ... | YEAR(date)_3 | HolidayCloseness_Distant | HolidayCloseness_Holiday | sin(1,365) | cos(1,365) | sin(2,365) | cos(2,365) | sin(3,365) | cos(3,365) | num_sold | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 2017-01-01 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ... | 0 | 0 | 1 | 0.000000e+00 | 1.000000 | 0.000000e+00 | 1.000000 | 0.000000e+00 | 1.000000 | 663 |

| 1 | 2017-01-02 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ... | 0 | 0 | 0 | 1.721336e-02 | 0.999852 | 3.442161e-02 | 0.999407 | 5.161967e-02 | 0.998667 | 514 |

| 2 | 2017-01-03 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ... | 0 | 0 | 0 | 3.442161e-02 | 0.999407 | 6.880243e-02 | 0.997630 | 1.031017e-01 | 0.994671 | 549 |

| 3 | 2017-01-04 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ... | 0 | 0 | 0 | 5.161967e-02 | 0.998667 | 1.031017e-01 | 0.994671 | 1.543088e-01 | 0.988023 | 477 |

| 4 | 2017-01-05 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ... | 0 | 1 | 0 | 6.880243e-02 | 0.997630 | 1.372788e-01 | 0.990532 | 2.051045e-01 | 0.978740 | 447 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 70123 | 2020-12-27 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 1 | ... | 1 | 0 | 0 | -6.880243e-02 | 0.997630 | -1.372788e-01 | 0.990532 | -2.051045e-01 | 0.978740 | 204 |

| 70124 | 2020-12-28 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 1 | ... | 1 | 0 | 0 | -5.161967e-02 | 0.998667 | -1.031017e-01 | 0.994671 | -1.543088e-01 | 0.988023 | 212 |

| 70125 | 2020-12-29 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 1 | ... | 1 | 1 | 0 | -3.442161e-02 | 0.999407 | -6.880243e-02 | 0.997630 | -1.031017e-01 | 0.994671 | 242 |

| 70126 | 2020-12-30 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 1 | ... | 1 | 1 | 0 | -1.721336e-02 | 0.999852 | -3.442161e-02 | 0.999407 | -5.161967e-02 | 0.998667 | 239 |

| 70127 | 2020-12-31 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 1 | ... | 1 | 1 | 0 | -9.797174e-16 | 1.000000 | -1.959435e-15 | 1.000000 | -2.939152e-15 | 1.000000 | 202 |

70128 rows × 69 columns

The feature matrix is almost ready for use in ARIMAX model. To summarize what we have done so far regarding the features, we have transformed the time points to categorical variables - day of the month, weekday, and year and added holidays. To better account for the effect of holidays, we have created three dummy holidays variables: Close, Distant and Holiday. Then to capture yearly seasonality we have added Fourier terms with period of 365. After creating the subset we can discard the country, product and store variables since we are training the models for each combination and they add nothing of value for forecasting in this case.

Let’s create the ARIMAX model and forecast with the same subset.

from statsmodels.tsa.arima.model import ARIMA

from statsmodels.tsa.statespace.sarimax import SARIMAX

# Create the same subset but this time with features.

subset_reg = feature_matrix[

(feature_matrix["country_Germany"] == 1)

& (feature_matrix["store_KaggleRama"] == 1)

& (feature_matrix["product_Kaggle Recipe Book"] == 1)

]

subset_reg = subset_reg.drop(

columns=[

"date",

"country_France",

"country_Germany",

"country_Poland",

"country_Italy",

"country_Spain",

"store_KaggleRama",

"product_Kaggle Getting Started",

"product_Kaggle Recipe Book",

"product_Kaggle for Kids: One Smart Goose",

]

)

# Train - Test Split

train_reg, test_reg = temporal_train_test_split(subset_reg, test_size=366)

# Define endogenous and exogenous variables

endog = train_reg["num_sold"]

exog = train_reg.drop(columns="num_sold")

# Use the same orders as previous ARIMA model

arimax_model = ARIMA(

order=(3, 1, 3), endog=endog, trend=[0, 1], exog=exog, enforce_stationarity=True

)

arimax_results = arimax_model.fit()

# Forecast for the last year

forecast_reg = arimax_results.forecast(366, exog=test_reg.drop(columns="num_sold"))

test_reg = test_reg.set_index(forecast_reg.index)

# Plot both test data and forecast from the model to compare them visually.

plot_forecasts(test_reg["num_sold"], forecast_reg, title="ARIMAX Forecasts");From the plot we can see that this model performs worse than STL-ARIMA model. Let’s check ARIMAX model’s MAPE score to quantify performance difference.

print(f"MAPE for ARIMAX model is: {mean_absolute_percentage_error(test_reg['num_sold'], forecast_reg)}")

print(f"R2 Score for ARIMAX model is: {r2_score(test_reg['num_sold'], forecast_reg)}")MAPE for ARIMAX model is: 0.6281181684643169

R2 Score for ARIMAX model is: -7.921475722370131Let’s try the regression now with using XGBoost. We will again use the same feature matrix as exogenous variables but we’ll also use previous values of num_sold as input variables.

from sklearn.preprocessing import MinMaxScaler

# Create a function so that we can try with different window sizes

def prev_values_tabularizer(feature_matrix, endog, window_size, scaler=False):

# Create a list to store previous values

prev_values = list()

for i in range(len(feature_matrix)):

prev_values.append(feature_matrix[endog][i : i + window_size])

# Reshape from columns to rows

prev_values = [

pandas.Series(prev_values[i]).values.reshape([1, -1])

for i in range(len(prev_values))

]

# Create placeholder DataFrame with zeros and change them with previous values

zeros_matrix = np.zeros(shape=[len(feature_matrix), window_size])

placeholder_df = pandas.DataFrame(zeros_matrix)

for i in range(len(placeholder_df)):

for j in range(window_size):

try:

placeholder_df[j][i] = prev_values[i][0][j]

except IndexError:

continue

# Add previous values to feature matrix, shift it by window size, remove first window size values from the feature matrix

feature_matrix = pandas.concat([feature_matrix, placeholder_df], axis=1)

feature_matrix[list(range(window_size))] = feature_matrix[

list(range(window_size))

].shift(window_size)

feature_matrix = feature_matrix.drop(list(range(window_size)), axis=0)

# If scaler is passed, apply scaling to previous values of endogenous variable

if scaler != False:

feature_matrix[list(range(window_size))] = scaler.fit_transform(

feature_matrix[list(range(window_size))]

)

# Reorder the columns so that endogenous variables are at the far most right

reordered_columns = (

feature_matrix.columns.to_list()[: (-window_size - 1)]

+ feature_matrix.columns.to_list()[(-window_size):]

+ [feature_matrix.columns.to_list()[(-window_size - 1)]]

)

feature_matrix = feature_matrix[reordered_columns]

return feature_matrix

scaler = MinMaxScaler()

# We use 7 as window_size because of the previous partial autocorrelation graphs

regression_matrix = prev_values_tabularizer(feature_matrix, "num_sold", 7)We have transformed the feature matrix suitable for forecasting with regression. Now we have to split it again to train and test subsets and create regression model with XGBoost.

from xgboost import XGBRegressor

# Create the same subset as previous examples and split

subset_xgboost = regression_matrix[

(regression_matrix["country_Germany"] == 1)

& (regression_matrix["store_KaggleRama"] == 1)

& (regression_matrix["product_Kaggle Recipe Book"] == 1)

]

subset_xgboost = subset_xgboost.drop(

columns=[

"date",

"country_France",

"country_Germany",

"country_Poland",

"country_Italy",

"country_Spain",

"store_KaggleRama",

"product_Kaggle Getting Started",

"product_Kaggle Recipe Book",

"product_Kaggle for Kids: One Smart Goose",

]

)

train_subset_xgboost, test_subset_xgboost = temporal_train_test_split(

subset_xgboost, test_size=366

)

# Define train/test features and targets

train_targets_xgboost = train_subset_xgboost["num_sold"]

train_features_xgboost = train_subset_xgboost.drop(columns="num_sold")

test_targets_xgboost = test_subset_xgboost["num_sold"]

test_features_xgboost = test_subset_xgboost.drop(columns="num_sold")

# Define model

xgboost_model = XGBRegressor()

xgboost_model.fit(train_features_xgboost, train_targets_xgboost)

# Forecast for the last year

forecast_xgboost = pandas.DataFrame(xgboost_model.predict(test_features_xgboost))

forecast_xgboost.set_index(test_features_xgboost.index, inplace=True)

# Plot both test data and forecast from the model to compare them visually.

plot_forecasts(test_targets_xgboost, forecast_xgboost, title="XGBoost Forecasts");From the plot we can see that regression model with XGBoost performs better than ARIMAX model. Let’s check the scores again.

print(f"MAPE for XGBoost Model is: {mean_absolute_percentage_error(test_targets_xgboost, forecast_xgboost)}")

print(f"R2 Score for XGBoost Model is: {r2_score(test_targets_xgboost, forecast_xgboost)}")MAPE for XGBoost Model is: 0.09307335208975362

R2 Score for XGBoost Model is: 0.6931165642563528Scores surely seems better than our other forecasting attempts with STL-ARIMA and ARIMAX, though it can be said that this regression model tends not to undershoot. It is also more successful to capture New Year’s Eve sales than other models.

It is still early to call this the best model, since we didn’t tuned thoroughly the models’ hyperparamaters and there are deep learning models to try. Now we’ll move to the business case definition and after that, hyperparameter tuning of STL-ARIMA, ARIMAX, and XGBoost models. For deep learning part of this case please refer to Part 2.

To compare different models, so far, we have used Mean Absolute Percentage Error and R2 Scores. We have also plotted our forecasts and compared them with test targets. Now we will approach the problem from a different perspective.

Instead of minimizing error, we will try to minimize our cost. It didn’t matter whether a sales forecast is for example 20 units more or less; but having 20 more books in the inventory and opportunity cost of selling 20 less books may not be the same. Our custom function will define exactly that.

Our assumptions are:

With these assumptions, one warehouse can store approximately 6000 books for a storage fee of €100 per month. The scenario is that for every each book which the forecast undershoots the true sales, we have the opportunity cost of one book. If the forecast overshoots the true sales, then we can store the book in our warehouse by renting it. After renting the warehouse, each subsequent undershoot can be compensated from our inventory - effectively eliminating the opportunity cost but if storage limit is exceeded then we have to rent another warehouse increasing our monthly cost to €200.

We will use the function cost_function() to calculate this metric.

# Define cost function for our case

def cost_function(storage, y_true, y_pred, book_price, storage_monthly_rent):

if storage == 0:

if y_pred <= y_true:

cost = book_price*(y_true - y_pred)

to_storage = 0

return cost, to_storage

elif y_pred > y_true:

cost = storage_monthly_rent/30

to_storage = y_pred - y_true

return cost, to_storage

elif storage > 0:

if y_pred <= y_true:

if (y_true - y_pred) < storage:

cost = storage_monthly_rent/30

to_storage = y_pred - y_true

return cost, to_storage

elif (y_true - y_pred) > storage:

cost = book_price*(y_true - y_pred - storage) + storage_monthly_rent/30

to_storage = -storage

return cost, to_storage

elif y_pred > y_true:

cost = storage_monthly_rent/30

to_storage = y_pred - y_true

return cost, to_storageNow we will tune and select hyperparameters for our models with the lowest cost. To reduce bias and get better generalization from the models, we will split the data to train - test - validation. While searching for the model with lowest cost using test data it may overfit. Therefore, we will tune the parameters using test dataset and after that check the performance using validation data.

Also earlier we were using test features for forecasts but feature matrix contains future num_sold values in it; thus, it wasn’t a legitimate forecast. In this part we will also change the way forecasts are created so that the model uses its own forecasts as past values instead of real sales.

import optuna

import statsmodels

# Create validation data for STL-Arima

train_subset = subset["num_sold"][0:730].reset_index().drop(columns="index")

test_subset = subset["num_sold"][730:1095].reset_index().drop(columns="index")

val_subset = subset["num_sold"][1095:1461].reset_index().drop(columns="index")

# Define Optuna Objective

def stl_objective(trial):

# Select ranges for p, d, q orders

p_order = trial.suggest_int("p_order", 0, 10, log=False)

d_order = trial.suggest_int("d_order", 0, 2, log=False)

q_order = trial.suggest_int("q_order", 0, 10, log=False)

robust_bool = trial.suggest_categorical("robust_mode", [False, True])

trend_deg = trial.suggest_int("trend_deg", 0, 1)

seasonal_deg = trial.suggest_int("seasonal_deg", 0, 1)

low_pass_deg = trial.suggest_int("low_pass_deg", 0, 1)

seasonal_jump = trial.suggest_int("seasonal_jump", 1, 3)

trend_jump = trial.suggest_int("trend_jump", 1, 3)

low_pass_jump = trial.suggest_int("low_pass_jump", 1, 3)

# Define model with trial variables

stl_forecast_tuned = STLForecast(

train_subset,

model=statsmodels.tsa.arima.model.ARIMA,

model_kwargs={"order": (p_order, d_order, q_order), "trend": "n"},

period=365,

trend=731,

trend_deg=trend_deg,

seasonal_deg=seasonal_deg,

low_pass_deg=low_pass_deg,

seasonal_jump=seasonal_jump,

trend_jump=trend_jump,

low_pass_jump=low_pass_jump,

robust=robust_bool,

)

# Fit and forecast test data

model = stl_forecast_tuned.fit()

forecast = model.forecast(steps=365)

# Reset index of forecasts

forecast = forecast.reset_index().drop(columns="index")

# Create a loop to calculate cumulative cost of the forecast

storage = 0

cumulative_cost = 0

book_price = 20

monthly_storage_cost = 100

for step in range(len(test_subset)):

# Get the cost and difference for storage for the current step

cost, to_storage = cost_function(

storage, test_subset["num_sold"][step], forecast[0][step], book_price, monthly_storage_cost

)

# Add cost to cumulative cost and storage difference to storage

cumulative_cost += int(cost)

storage += int(to_storage)

total_cost = cumulative_cost + storage * book_price

return total_cost

# Create Optuna Study and Minimize total_cost

stl_study = optuna.create_study(direction="minimize")

stl_study.optimize(stl_objective, n_trials=20)Now we’ll create the model with best parameters to get tuned forecasts.

# Get the parameters of the best model

best_stl_model_parameters = stl_study.best_params

# Define STL-Arima model with the best parameters and train on test data

stl_forecast = STLForecast(

test_subset,

model=statsmodels.tsa.arima.model.ARIMA,

model_kwargs={

"order": (

best_stl_model_parameters["p_order"],

best_stl_model_parameters["d_order"],

best_stl_model_parameters["q_order"],

),

"trend": "n",

},

period=365,

trend=1095,

robust=best_stl_model_parameters["robust_mode"],

trend_deg=best_stl_model_parameters["trend_deg"],

seasonal_deg=best_stl_model_parameters["seasonal_deg"],

low_pass_deg=best_stl_model_parameters["low_pass_deg"],

seasonal_jump=best_stl_model_parameters["seasonal_jump"],

trend_jump=best_stl_model_parameters["trend_jump"],

low_pass_jump=best_stl_model_parameters["low_pass_jump"],

)

# Fit and forecast test data

tuned_stl_model = stl_forecast.fit()

forecast_stl_arima_tuned = tuned_stl_model.forecast(steps=366)

forecast_stl_arima_tuned = forecast_stl_arima_tuned.reset_index().drop(columns="index")

# Create a loop to calculate cumulative cost of the forecast

storage = 0

cumulative_cost = 0

book_price = 20

monthly_storage_cost = 100

for step in range(len(val_subset)):

# Get the cost and difference for storage for the current step

cost, to_storage = cost_function(

storage,

val_subset["num_sold"][step],

forecast_stl_arima_tuned[0][step],

book_price,

monthly_storage_cost,

)

# Add cost to cumulative cost and storage difference to storage

cumulative_cost += int(cost)

storage += int(to_storage)

stl_arima_total_cost = cumulative_cost + storage * book_price

# Plot both test data and forecast from the model to compare them visually.

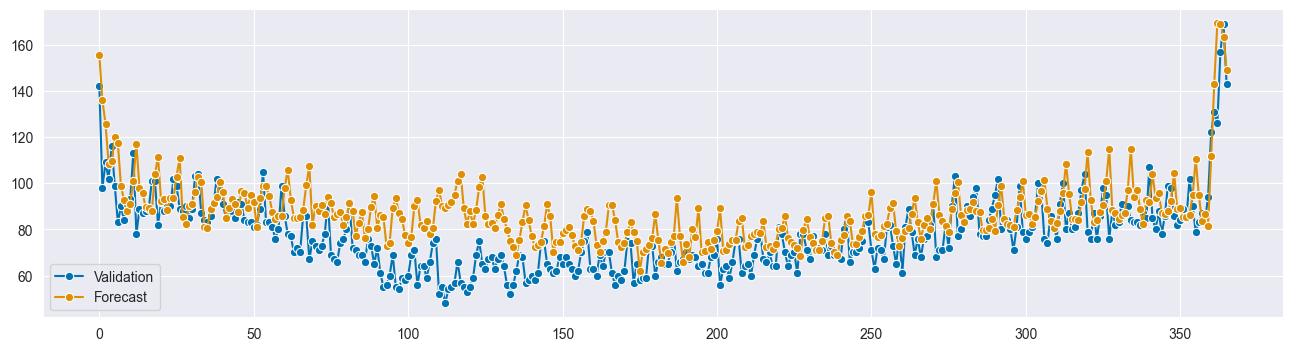

plot_forecasts(val_subset, forecast_stl_arima_tuned, title="STL ARIMA Tuned Forecasts");Calculate the MAPE and R2 Scores and the total cost according to our metric.

print(f"MAPE for Earlier STL-ARIMA Model is: {mean_absolute_percentage_error(test_subset_pretuning, forecast)}")

print(f"MAPE for Tuned STL-ARIMA is: {mean_absolute_percentage_error(val_subset['num_sold'], forecast_stl_arima_tuned[0])}\n")

print(f"R2 Score for Earlier STL-ARIMA Model is: {r2_score(test_subset_pretuning, forecast)}")

print(f"R2 Score for Tuned STL-ARIMA is: {r2_score(val_subset['num_sold'], forecast_stl_arima_tuned[0])}\n")

print(f"Total Cost for tuned STL-ARIMA is: €{stl_arima_total_cost:,.2f}")MAPE for Earlier STL-ARIMA Model is: 0.18646794982275017

MAPE for Tuned STL-ARIMA is: 0.16666477586835288

R2 Score for Earlier STL-ARIMA Model is: -0.6091132358371121

R2 Score for Tuned STL-ARIMA is: 0.037154861121782456

Total Cost for tuned STL-ARIMA is: €72,474.00# Create validation data for ARIMAX

train_subset = subset[0:730]

test_subset = subset[730:1095]

val_subset = subset[1095:1461]

# Define endogenous and exogenous variables

train_targets = pandas.DataFrame(train_subset["num_sold"]).reset_index().drop(columns="index")

train_features = pandas.DataFrame(train_subset.drop(columns="num_sold")).reset_index().drop(columns="index")

test_targets = pandas.DataFrame(test_subset["num_sold"]).reset_index().drop(columns="index")

test_features = pandas.DataFrame(test_subset.drop(columns="num_sold")).reset_index().drop(columns="index")

val_targets = pandas.DataFrame(val_subset["num_sold"]).reset_index().drop(columns="index")

val_features = pandas.DataFrame(val_subset.drop(columns="num_sold")).reset_index().drop(columns="index")

# Define Optuna Objective

def arimax_objective(trial):

# Select ranges for p, d, q orders

p_order = trial.suggest_int("p_order", 0, 10, log=False)

d_order = trial.suggest_int("d_order", 0, 2, log=False)

q_order = trial.suggest_int("q_order", 0, 10, log=False)

# Trend order according to d_order differencing

trend_order = list(np.zeros(d_order))

trend_order.append(1)

# Define model with trial variables

arimax_model = statsmodels.tsa.arima.model.ARIMA(

order=(p_order, d_order, q_order),

endog=train_targets,

trend=trend_order,

exog=train_features

)

# Fit the model

arimax_model_results = arimax_model.fit()

# Forecast for the last year

forecast_arimax_tuned = arimax_model_results.forecast(365, exog=test_features)

forecast_arimax_tuned = pandas.DataFrame(forecast_arimax_tuned).reset_index().drop(columns="index")

# Create a loop to calculate cumulative cost of the forecast

storage = 0

cumulative_cost = 0

book_price = 20

monthly_storage_cost = 100

for step in range(len(test_targets)):

# Get the cost and difference for storage for the current step

cost, to_storage = cost_function(

storage,

test_targets["num_sold"][step],

forecast_arimax_tuned["predicted_mean"][step],

book_price,

monthly_storage_cost

)

# Add cost to cumulative cost and storage difference to storage

cumulative_cost += int(cost)

storage += int(to_storage)

total_cost = cumulative_cost + storage*book_price

return total_cost

# Create Optuna Study and Minimize total_cost

arimax_study = optuna.create_study(direction="minimize")

arimax_study.optimize(arimax_objective, n_trials=20)# Get the parameters of the best model

best_arimax_model_parameters = arimax_study.best_params

# Trend order according to d_order differencing

trend_order = list(np.zeros(best_arimax_model_parameters["d_order"]))

trend_order.append(1)

# Define Arimax model with the best parameters and train on test data

arimax_model = statsmodels.tsa.arima.model.ARIMA(

order=(best_arimax_model_parameters["p_order"],

best_arimax_model_parameters["d_order"],

best_arimax_model_parameters["q_order"]),

endog=test_targets,

trend=[0],

exog=test_features)

# Fit the model

arimax_model_results = arimax_model.fit()

# Forecast for the last year

forecast_arimax_tuned = arimax_model_results.forecast(366, exog=val_features)

forecast_arimax_tuned = pandas.DataFrame(forecast_arimax_tuned).reset_index().drop(columns="index")

# Create a loop to calculate cumulative cost of the forecast

storage = 0

cumulative_cost = 0

book_price = 20

monthly_storage_cost = 100

for step in range(len(val_targets)):

# Get the cost and difference for storage for the current step

cost, to_storage = cost_function(

storage,

val_targets["num_sold"][step],

forecast_arimax_tuned["predicted_mean"][step],

book_price,

monthly_storage_cost)

# Add cost to cumulative cost and storage difference to storage

cumulative_cost += int(cost)

storage += int(to_storage)

arimax_total_cost = cumulative_cost + storage*book_price

# Plot both test data and forecast from the model to compare them visually.

plot_forecasts(val_targets, forecast_arimax_tuned, title="ARIMAX Tuned Forecasts");print(f"MAPE for Earlier ARIMAX model is: {mean_absolute_percentage_error(test_reg['num_sold'], forecast_reg)}")

print(f"MAPE for Tuned ARIMAX model is: {mean_absolute_percentage_error(val_targets['num_sold'], forecast_arimax_tuned['predicted_mean'])}\n")

print(f"R2 Score for Earlier ARIMAX model is: {r2_score(test_reg['num_sold'], forecast_reg)}")

print(f"R2 Score for Tuned ARIMAX model is: {r2_score(val_targets['num_sold'], forecast_arimax_tuned['predicted_mean'])}\n")

print(f"Total Cost for tuned ARIMAX model is: €{arimax_total_cost:,.2f}")MAPE for Earlier ARIMAX model is: 0.6281181684643169

MAPE for Tuned ARIMAX model is: 0.8729066657738429

R2 Score for Earlier ARIMAX model is: -7.921475722370131

R2 Score for Tuned ARIMAX model is: -17.11867129518898

Total Cost for tuned ARIMAX model is: €484,567.00from xgboost import XGBRegressor

# Create train - test- validation data

subset_xgboost_tuned = regression_matrix[

(regression_matrix["country_Germany"] == 1)

& (regression_matrix["store_KaggleRama"] == 1)

& (regression_matrix["product_Kaggle Recipe Book"] == 1)

]

subset_xgboost_tuned = subset_xgboost_tuned.drop(

columns=[

"date",

"country_France",

"country_Germany",

"country_Poland",

"country_Italy",

"country_Spain",

"store_KaggleRama",

"product_Kaggle Getting Started",

"product_Kaggle Recipe Book",

"product_Kaggle for Kids: One Smart Goose",

]

)

# Define train - test - validation features and targets

train_subset_xgboost_tuned, test_subset_xgboost_tuned = temporal_train_test_split(

subset_xgboost_tuned, train_size=730

)

test_subset_xgboost_tuned, val_subset_xgboost_tuned = temporal_train_test_split(

test_subset_xgboost_tuned, test_size=366

)

train_targets_xgboost_tuned = (

pandas.DataFrame(train_subset_xgboost_tuned["num_sold"])

.reset_index()

.drop(columns="index")

)

train_features_xgboost_tuned = (

pandas.DataFrame(train_subset_xgboost_tuned.drop(columns="num_sold"))

.reset_index()

.drop(columns="index")

)

test_targets_xgboost_tuned = (

pandas.DataFrame(test_subset_xgboost_tuned["num_sold"])

.reset_index()

.drop(columns="index")

)

test_features_xgboost_tuned = (

pandas.DataFrame(test_subset_xgboost_tuned.drop(columns="num_sold"))

.reset_index()

.drop(columns="index")

)

val_targets_xgboost_tuned = (

pandas.DataFrame(val_subset_xgboost_tuned["num_sold"])

.reset_index()

.drop(columns="index")

)

val_features_xgboost_tuned = (

pandas.DataFrame(val_subset_xgboost_tuned.drop(columns="num_sold"))

.reset_index()

.drop(columns="index")

)

# Define forecasting function

def regression_forecast(

train_features, forecast_features, model, window_size, scaled=False

):

# Add the last column of training data

history = train_features.tail(1)

forecasts = list()

for _ in range(len(forecast_features)):

prediction = model.predict(history.tail(1))

# Get features of data to be forecasted

next_sample = forecast_features.head(1)

# Shift previous values to 1 left

next_sample[list(range(window_size))] = (

history.tail(1)[list(range(window_size))].shift(-1, axis=1).values

)

# If scaled, inverse transform

if scaled != False:

next_sample[list(range(window_size))] = scaler.inverse_transform(

next_sample[list(range(window_size))]

)

# Add prediction to the right

next_sample[window_size - 1] = prediction

# Scale values again before forecasting

next_sample[list(range(window_size))] = scaler.transform(

next_sample[list(range(window_size))]

)

else:

# Add prediction to the right

next_sample[window_size - 1] = prediction

# Add last values to history

history = pandas.concat([history, next_sample], ignore_index=True, axis=0)

# Drop uppermost row from forecast features

forecast_features = forecast_features.drop(index=min(forecast_features.index))

# Add current prediction the forecasts as a seperate list

forecasts.append(prediction)

return pandas.DataFrame(forecasts, columns=["prediction"])

# Define Optuna Objective

def xgboost_objective(trial):

# Define trial variables

booster = trial.suggest_categorical("booster", ["gbtree", "gblinear", "dart"])

if booster in ["gbtree", "dart"]:

eta = trial.suggest_float("eta", 0, 1)

gamma = trial.suggest_int("gamma", 0, 2)

max_depth = trial.suggest_int("max_depth", 1, 50)

min_child_weight = trial.suggest_int("min_child_weight", 0, 20)

subsample = trial.suggest_float("subsample", 0.5, 1)

reg_lambda = trial.suggest_float("lambda", 0, 5)

alpha = trial.suggest_float("alpha", 0, 5)

# Define model with trial variables

xgboost_model = XGBRegressor(

booster=booster,

learning_rate=eta,

min_split_loss=gamma,

max_depth=max_depth,

min_child_weight=min_child_weight,

subsample=subsample,

reg_lambda=reg_lambda,

reg_alpha=alpha,

)

else:

reg_lambda = trial.suggest_float("lambda", 0, 5)

alpha = trial.suggest_float("alpha", 0, 5)

updater = trial.suggest_categorical("updater", ["shotgun", "coord_descent"])

feature_selector = trial.suggest_categorical(

"feature_selector", ["cyclic", "shuffle"]

)

# Define model with trial variables

xgboost_model = XGBRegressor(

booster=booster,

reg_lambda=reg_lambda,

reg_alpha=alpha,

updater=updater,

feature_selector=feature_selector,

)

# Fit the model

xgboost_model.fit(train_features_xgboost_tuned, train_targets_xgboost_tuned)

# Forecast for the test data but this time using model's predicted values as past values

forecast_xgboost_tuned = regression_forecast(

train_features_xgboost_tuned,

test_features_xgboost_tuned,

xgboost_model,

7

)

# Create a loop to calculate cumulative cost of the forecast

storage = 0

cumulative_cost = 0

book_price = 20

monthly_storage_cost = 100

for step in range(len(test_targets_xgboost_tuned)):

# Get the cost and difference for storage for the current step

cost, to_storage = cost_function(

storage,

test_targets_xgboost_tuned["num_sold"][step],

forecast_xgboost_tuned["prediction"][step],

book_price,

monthly_storage_cost,

)

# Add cost to cumulative cost and storage difference to storage

cumulative_cost += int(cost)

storage += int(to_storage)

total_cost = cumulative_cost + storage * book_price

return total_cost

# Create Optuna Study and Minimize total_cost

xgboost_study = optuna.create_study(direction="minimize")

xgboost_study.optimize(xgboost_objective, n_trials=20)best_xgboost_model_parameters = xgboost_study.best_params

if best_xgboost_model_parameters["booster"] in ["gbtree", "dart"]:

# Define model with trial variables

xgboost_model = XGBRegressor(

booster=best_xgboost_model_parameters["booster"],

learning_rate=best_xgboost_model_parameters["eta"],

min_split_loss=best_xgboost_model_parameters["gamma"],

max_depth=best_xgboost_model_parameters["max_depth"],

min_child_weight=best_xgboost_model_parameters["min_child_weight"],

subsample=best_xgboost_model_parameters["subsample"],

reg_lambda=best_xgboost_model_parameters["lambda"],

reg_alpha=best_xgboost_model_parameters["alpha"]

)

else:

# Define model with trial variables

xgboost_model = XGBRegressor(

booster=best_xgboost_model_parameters["booster"],

reg_lambda=best_xgboost_model_parameters["lambda"],

reg_alpha=best_xgboost_model_parameters["alpha"],

updater=best_xgboost_model_parameters["updater"],

feature_selector=best_xgboost_model_parameters["feature_selector"]

)

# Fit the model with the best parameters

xgboost_model.fit(test_features_xgboost_tuned, test_targets_xgboost_tuned)

# Forecast for the test data but this time using model's predicted values as past values

forecast_xgboost_tuned = regression_forecast(

test_features_xgboost_tuned,

val_features_xgboost_tuned,

xgboost_model,

7)

# Create a loop to calculate cumulative cost of the forecast

storage = 0

cumulative_cost = 0

book_price = 20

monthly_storage_cost = 100

for step in range(len(val_targets_xgboost_tuned)):

# Get the cost and difference for storage for the current step

cost, to_storage = cost_function(

storage,

val_targets_xgboost_tuned["num_sold"][step],

forecast_xgboost_tuned["prediction"][step],

book_price,

monthly_storage_cost)

# Add cost to cumulative cost and storage difference to storage

cumulative_cost += int(cost)

storage += int(to_storage)

xgboost_total_cost = cumulative_cost + storage*book_price

# Plot the forecasts compared to validation data

plot_forecasts(val_targets_xgboost_tuned, forecast_xgboost_tuned, title="XGBoost Tuned Forecasts");print(f"MAPE for Earlier XGBoost model is: {mean_absolute_percentage_error(test_targets_xgboost, forecast_xgboost)}")

print(f"MAPE for Tuned XGBoost model is: {mean_absolute_percentage_error(val_targets_xgboost_tuned, forecast_xgboost_tuned)}\n")

print(f"R2 Score for Earlier XGBoost model is: {r2_score(test_targets_xgboost, forecast_xgboost)}")

print(f"R2 Score for Tuned XGBoost model is: {r2_score(val_targets_xgboost_tuned, forecast_xgboost_tuned)}\n")

print(f"Total Cost for Tuned XGBoost model is: €{xgboost_total_cost:,.2f}")MAPE for Earlier XGBoost model is: 0.09307335208975362

MAPE for Tuned XGBoost model is: 0.1657821900657774

R2 Score for Earlier XGBoost model is: 0.6931165642563528

R2 Score for Tuned XGBoost model is: 0.10051546999689664

Total Cost for Tuned XGBoost model is: €60,058.00Tuning for XGBoost model loses some accuracy due to the difference between lagged value features. Earlier model was using real targets as lagged value, while this tuned and correct model uses its own forecasts as lagged values. We’ll create and tune deep learning models on